Market Update Week 43

Weekly Market Recap - key stats

- Services and manufacturing PMIs both inched up

- Consumer Sentiment improved to 70.5 (scale is 1-100, over 50 is positive)

The week ahead

- Jobs report

- 3Q GDP

- PCE (Personal Consumption Expenditures - a spending report closely watched by the Fed.)

- Nonfarm Payrolls (another jobs report)

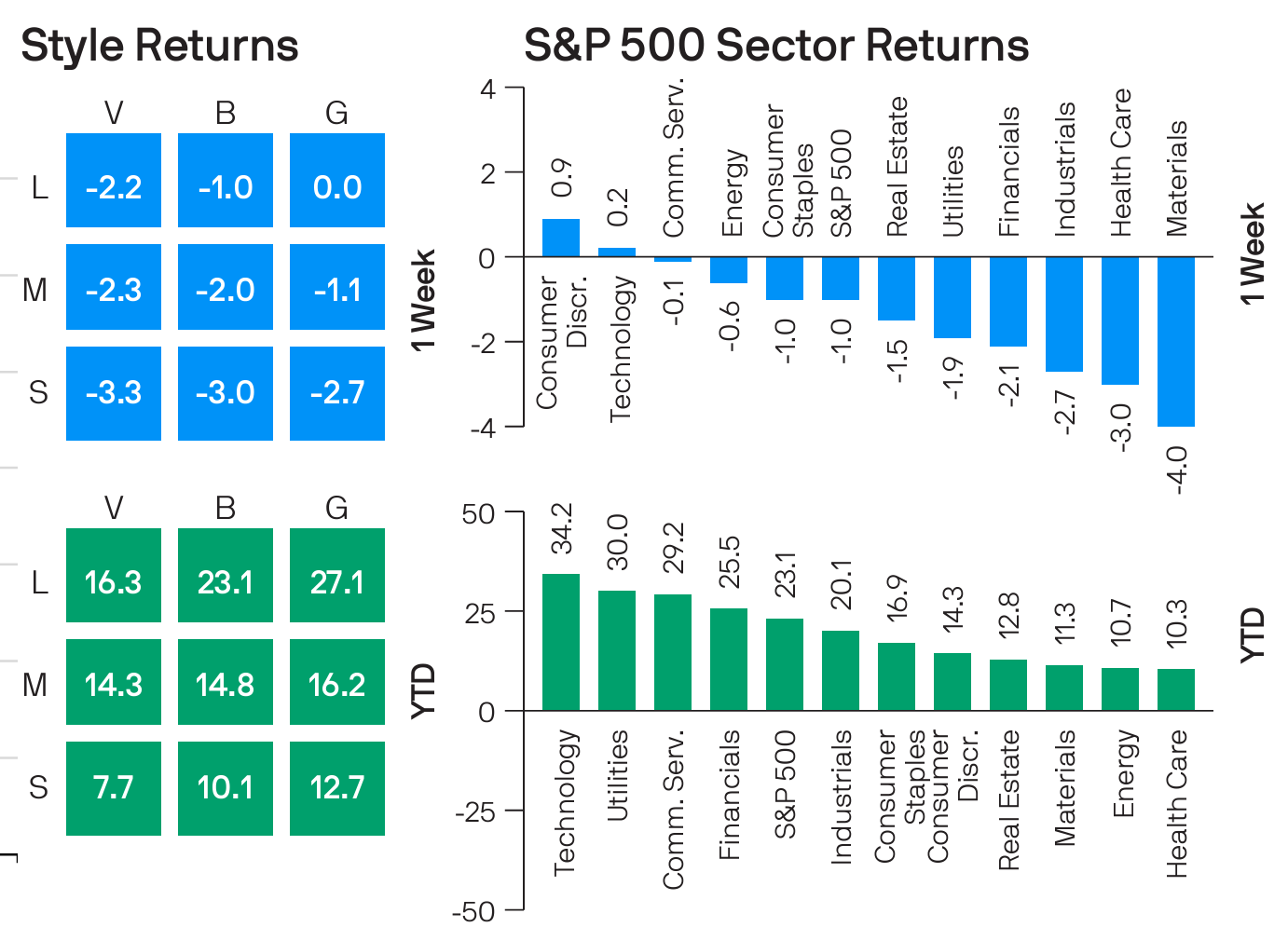

The S&P 500 index slipped 1% for its first weekly decline since early September as investors dissected companies' quarterly results.

The market benchmark ended the week at 5,808.12, its first weekly decline since the seven days ending Sept. 6. However, it's still up 0.8% this month and 22% in 2024.

Thought of the week

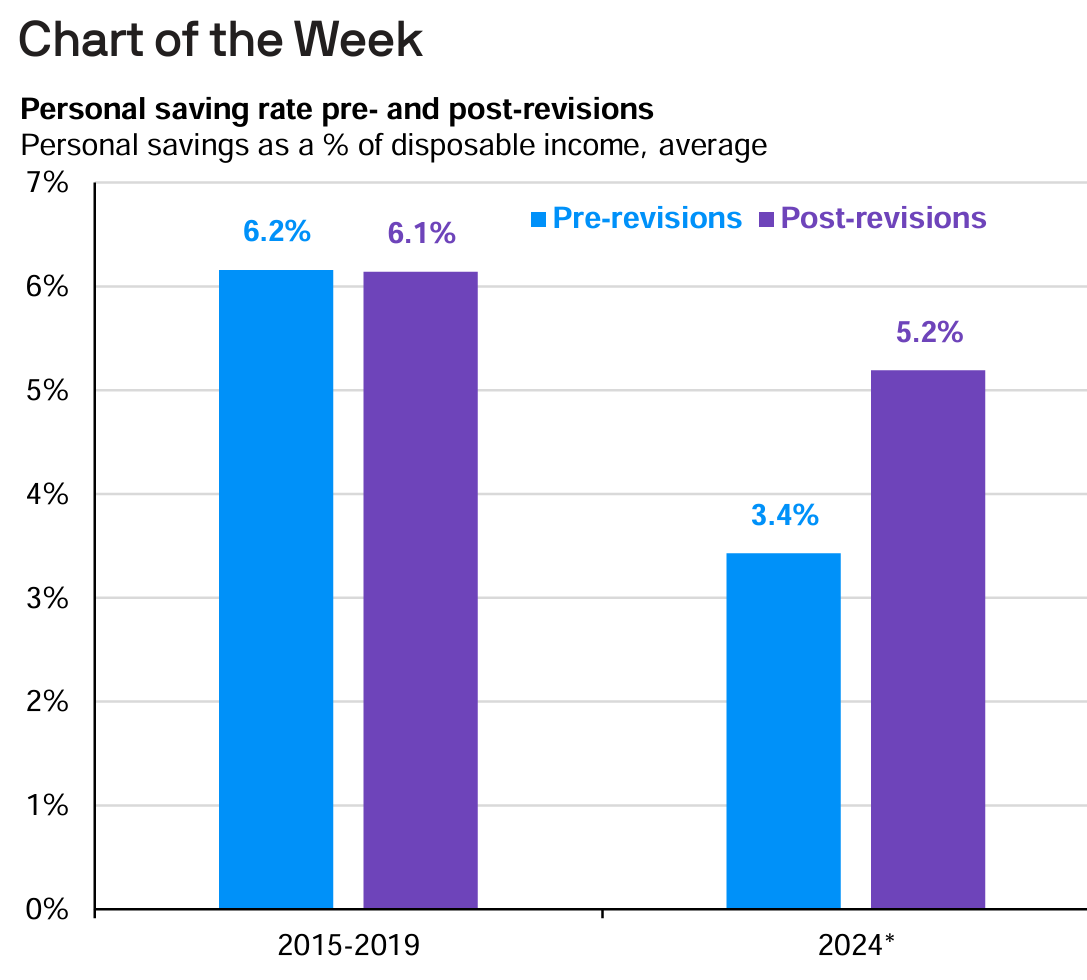

In a year with growth, inflation, interest rate, fiscal and geopolitical uncertainty, there has been one thing to count on: the American consumer. Despite rising delinquencies and data that until recently showed a historically low saving rate, consumer spending has defied expectations of a slowdown. In September, the Bureau of Economic Analysis's (BEA) annual revisions to the national income and product accounts may explain why.

This week’s chart shows the average personal saving rate in the five years before the pandemic compared to 2024, both before and after the BEA’s annual revisions. Prior to revisions, the personal saving rate averaged a record low of 3.4%, leading many to believe that spending was set to stall as consumers rebuilt their depleted savings. After revisions, however, the average personal saving rate jumped to 5.2%. While still below the average in the five years before the pandemic, this implies that consumers are in better financial shape than initially anticipated.

Note that here at Your Best Path, we noted several times that consumer reserves (cash, savings accounts, CDs, etc.) were above the pre-pandemic trend, so adding a lot more to savings didn't make a lot of sense for many households.

Ahead of a first look at third-quarter GDP, investors can find some peace of mind knowing that, in aggregate, consumers look healthy. However, there is divergence beneath the surface. Rising wealth has supported strong spending in the higher-income cohorts, while lower-income households remain under pressure. Still, bolstered by 17 straight months of positive year-over-year real wage gains, consumers should continue spending at a healthy pace, allowing the U.S. economy to maintain a soft landing into next year. Moving forward, resilient consumption should support earnings, allowing equities to grind higher, and a stable economy should allow the Federal Reserve to ease policy methodically.

Up Next

Next week's earnings calendar features Google parent Alphabet (GOOG, GOOGL), Visa (V), Advanced Micro Devices (AMD), McDonald's (MCD), Pfizer (PFE), Microsoft (MSFT), Facebook parent Meta Platforms (META), Eli Lilly (LLY), AbbVie (ABBV), Caterpillar (CAT), Apple (AAPL), Amazon.com (AMZN), Mastercard (MA), Merck (MRK), Berkshire Hathaway (BRK.A), Exxon Mobil (XOM) and Chevron (CVX).

In economic data, all eyes will be on October employment data, with ADP's private-sector report expected on Wednesday and the Labor Department's monthly nonfarm payrolls and unemployment rate due on Friday. Other highlights will include the release of Q3 gross domestic product on Tuesday and October personal consumption expenditures on Thursday.

All the Best,

Gordon Achtermann, CSRIC®, MBA, CFP®

Gordon@yourbestpathfp.com

703-573-7325

Your Best Path Financial Planning delivers comprehensive planning and investment management to families and individuals, whether you live in Fairfax, Virginia, Northern Virginia, or nationwide.