Market Update Week 46

Market Recap

Week of Nov.11 through Nov.15

The week in review

Headline CPI (Consumer Price Index) rose 0.2% m/m (2.6% y/y)

Headline PPI (Producer Price Index) also rose 0.2% m/m (2.4% y/y)

Retail sales rose 0.4% m/m

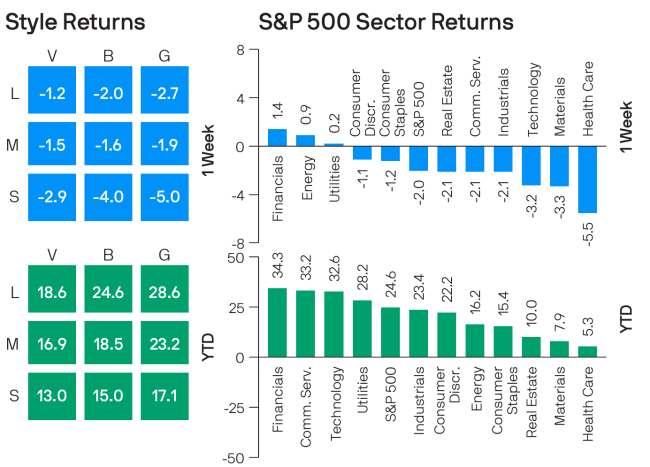

The S&P 500 index fell 2.1% this week as stronger-than-expected retail sales and comments by Federal Reserve Chair Jerome Powell led to reduced expectations for a December rate cut.

The market benchmark ended Friday's session at 5,870.62. Despite the weekly loss, the index is still up 2.9% for the month to date, thanks to a rally last week in reaction to the US presidential election and a Fed rate cut of 25 basis points. It is now up 23% for 2024.

Data on Friday showed US retail sales increased more than expected in October, aided by a jump in auto purchases, while the September reading saw an upward revision. The report contributed to lower expectations for a Fed rate cut, especially as it came a day after Fed Chair Powell said, "The economy is not sending any signals that we need to be in a hurry to lower rates."

Healthcare stocks led the broad decline, falling 5.5%, followed by a 3.3% drop in materials and a 3.2% loss in technology. Industrials, real estate, and communication services also shed at least 2% each.

The healthcare sector was weighed down by concerns about President-elect Donald Trump's nominee for health and human services secretary, Robert F. Kennedy Jr., given that Kennedy is a vaccine skeptic. Vaccine maker Moderna (MRNA) had the largest percentage drop in the sector, tumbling 21% from a week ago.

Just two sectors managed to eke out gains for the week: Financials rose 1.4%, and energy edged up 0.6%.

Gainers in the financial sector included shares of Charles Schwab (SCHW), which rose 9.1% on the week as the company reported its total client assets reached $9.85 trillion in October, up 29% year-over-year and down 1% sequentially. Following the report, the stock received price target increases from analysts at Wolfe Research, Citigroup, Deutsche Bank, and UBS.

Next Up

The week ahead will feature multiple housing reports, with November home builder confidence data due on Monday, October housing starts and building permits on Tuesday, and October existing home sales on Thursday. A final reading on November consumer sentiment is expected on Friday.

Charts

Commenting on the above chart, JP Morgan Asset Management reported, "Several of Trump’s top priorities are somewhat inflationary. Immigration restrictions could re-heat the labor market, stoking wage growth, and tariffs could increase prices. This, combined with a potential trade-war supply chain disruption, could reverse recent disinflation progress in goods."

Since firms like JPM never say anything without excessive modulation, this is as clear a warning as we are likely to ever get from them.

As you can see above, all of the floating US rates are up since the election, undoing virtually all of the rate progress made over the last year. 30-year mortgages have jumped 65 basis points since the last reading before the election, which will put a real damper on the housing industry.

All the Best,

Gordon Achtermann, CSRIC®, MBA, CFP®

Gordon@yourbestpathfp.com

703-573-7325

Your Best Path Financial Planning delivers comprehensive planning and investment management to families and individuals, whether you live in Fairfax, Virginia, Northern Virginia, or nationwide.