Market Update Week 42

Weekly Market Recap - key stats

- Retail sales rose 0.4% since last month (month/month or m/m)

- Housing starts were down - 0.5% m/m

- The ECB (European Central Bank) cut rates by 25 bps (1/4 of a %) (By keeping their rates below those in the US they keep the Euro weak, which helps their trade balance.)

The week ahead

- Markit PMIs (Purchasing Manager's Index)

- Durable goods orders

- Consumer sentiment

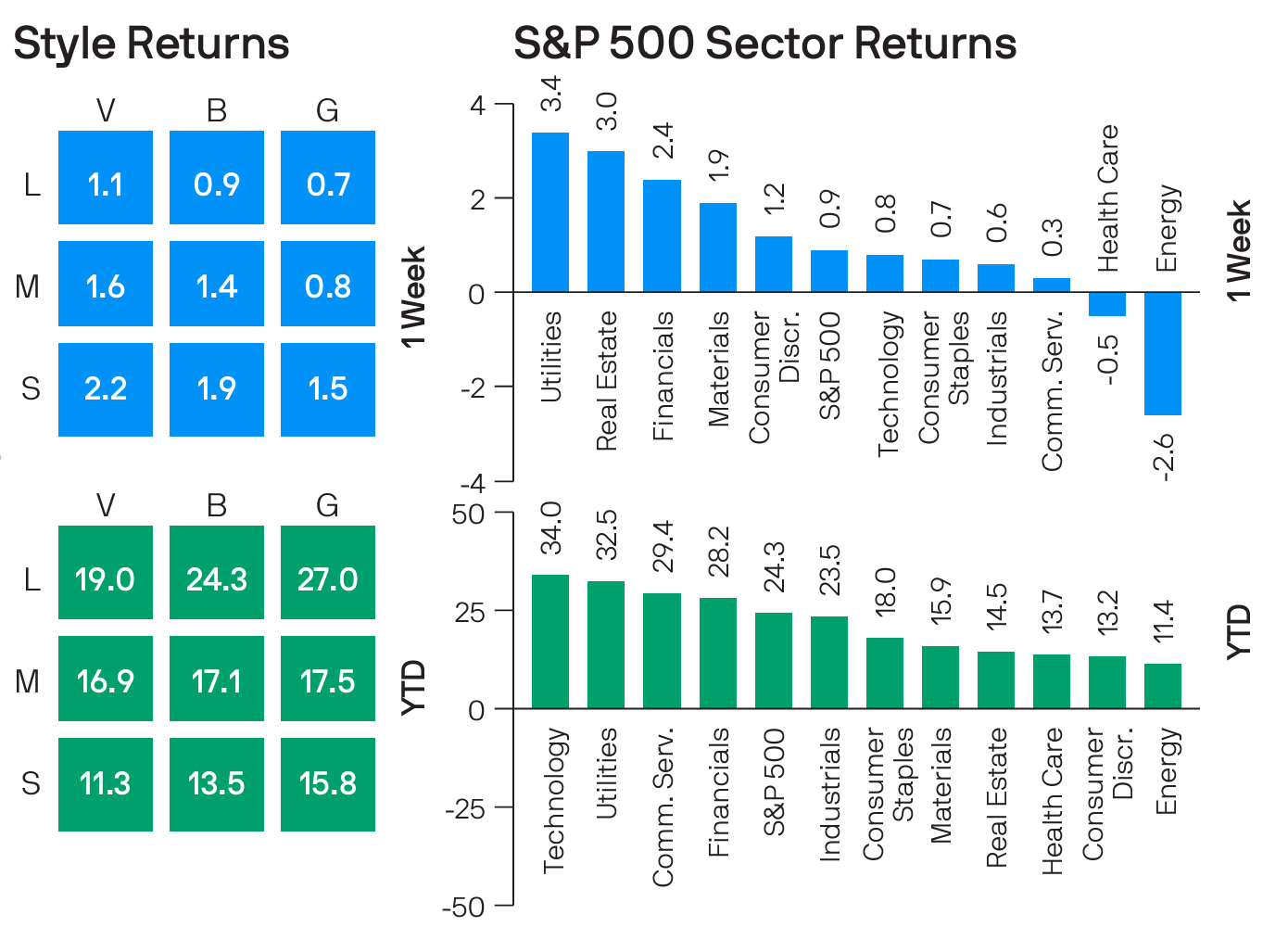

The S&P 500 index rose 0.9% this week, its sixth consecutive weekly gain, as a number of heavyweight US companies released quarterly results that topped expectations.

Thought of the Week

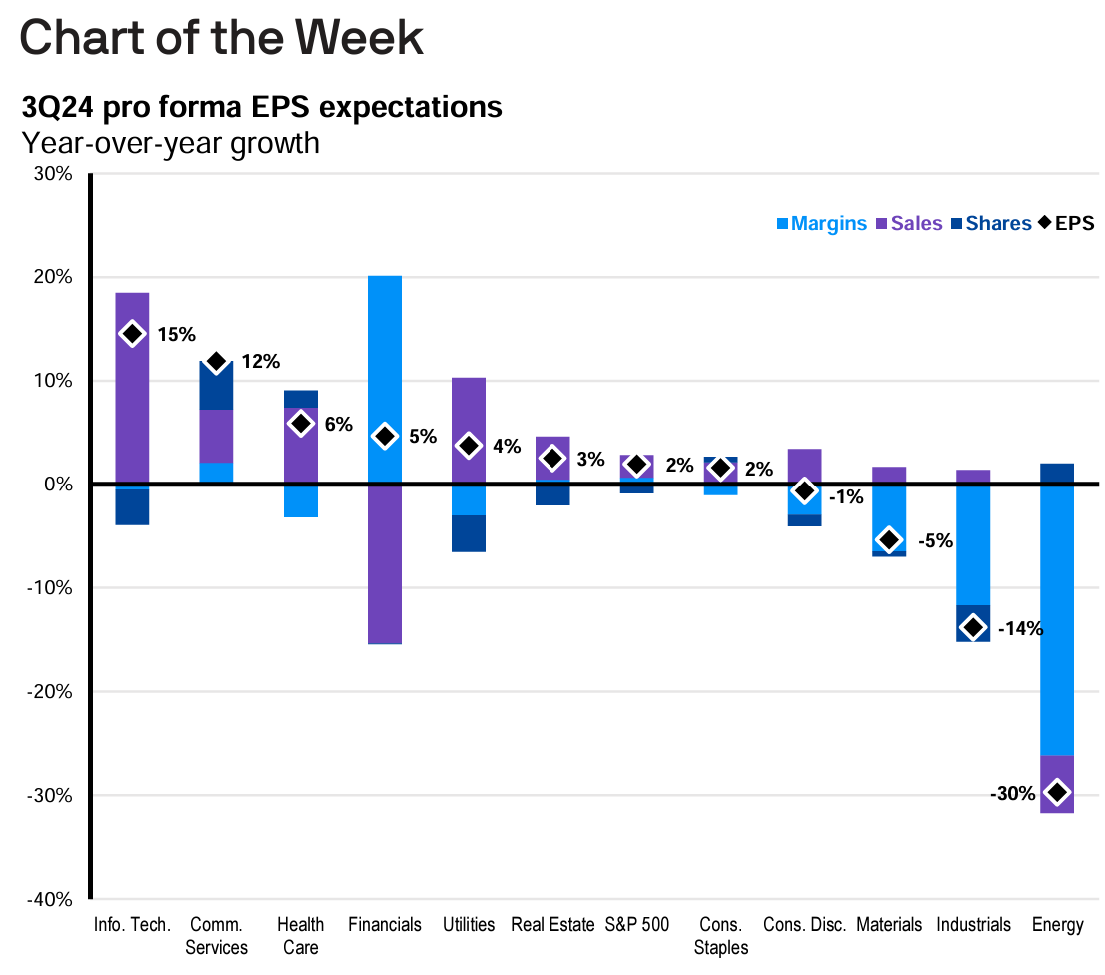

On the Expectations for 3Q EPS

The 3Q earnings season began Friday with reports from the largest U.S. banks. Currently, analysts are projecting pro forma earnings per share (EPS) of $60.01. If realized, this would represent y/y growth of 1.9% and a q/q contraction of -0.9%. Looking at the three main sources of EPS growth, revenues, margins and buybacks are expected to contribute 2.2, 0.5 and -0.8points, respectively.

Zooming out, the macro picture is still good for stocks, though growth and inflation have slowed from breakneck paces.The Atlanta Fed’s GDP Now model is projecting 3Q24 GDP growthof 3.2% annualized, and consumer spending seems similarly resilient with y/y growth tracking at 2% for goods and 3% for services. Manufacturing activity, however, remains weak with PMIs close to cycle lows. So, while growth sectors like Information Technology, Communication Services and Health Care should experience another quarter of robust earnings growth, cyclicals like Materials, Industrials and Energy are struggling.

Over the quarter, crude oil and natural gas prices decreased y/y by an average of 5.0% and 16.4%, respectively, hurting Energy sector profitability. In Industrials, transportation and capital goods activity is muted as companies postpone expenditures until interest rate and regulatory uncertainty dissipates. China’s centrality in global manufacturing and commodity demand is also hurting, particularly in Materials. But things are looking up. China’s stimulus, U.S. monetary easing and fiscal spending on energy and supply chain security should support a cyclical recovery. Indeed, all three sectors are expected to see double digit earnings growth by the second half of 2025.

All the Best,

Gordon Achtermann, CSRIC®, MBA, CFP®

Gordon@yourbestpathfp.com

703-573-7325

Your Best Path Financial Planning delivers comprehensive planning and investment management to families and individuals, whether you live in Fairfax, Virginia, Northern Virginia, or nationwide.