Market Update Week 52

Market Recap

Week of Dec. 23 through Dec. 27, 2024

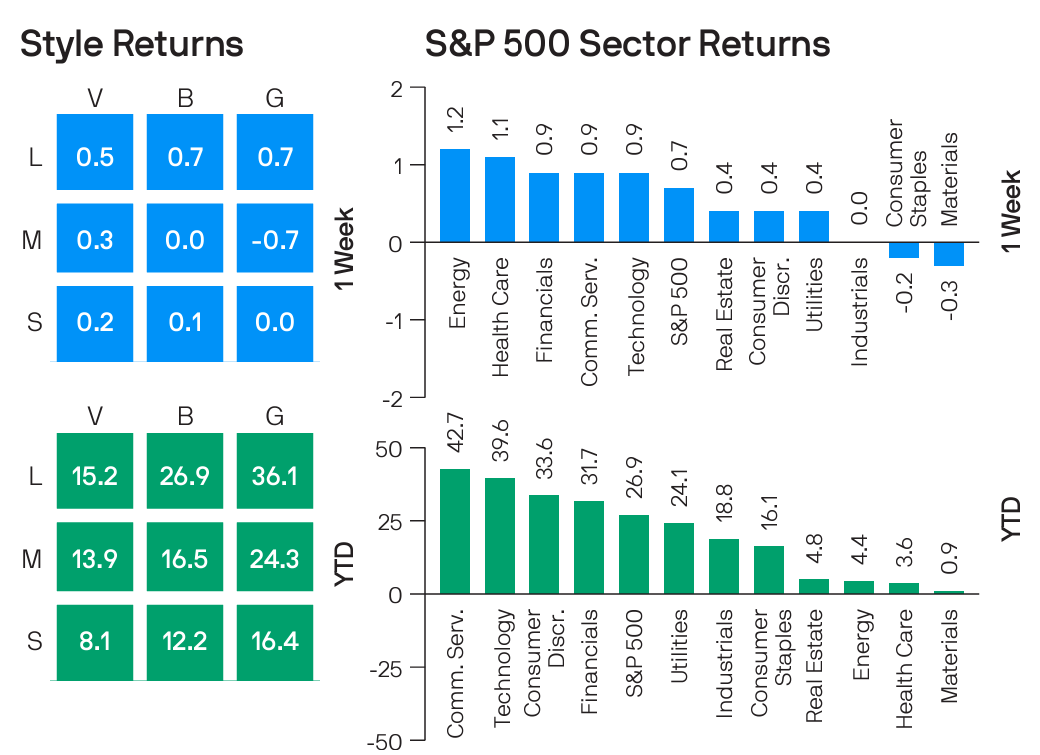

The S&P 500 avoided a third straight weekly loss, rising 0.7% and bringing its year-to-date gains to 25% with two trading days remaining in 2024.

The benchmark equity index ended Friday's session at 5,970.84, up from last week's close of 5,930.85. The S&P 500 closed at an all-time high of 6,090.3 on Dec. 6. Tuesday will be the last trading day of the year.

The effect of a so-called "Santa Claus" rally in the US stock market could reverse early next year amid the prospect of new trade policies or tariffs under the incoming Trump administration, Saxo Bank said in a report published this week. The Santa rally refers to the tendency for stock markets to move higher during the last week of December and the first two trading days of January.

US markets were closed Wednesday for Christmas. Retail sales increased more than expected during the holiday season and came in above last year's growth pace, according to preliminary data from a Mastercard (MA) report. However, consumer confidence fell to 104.7 in December.

Thought of the Week*

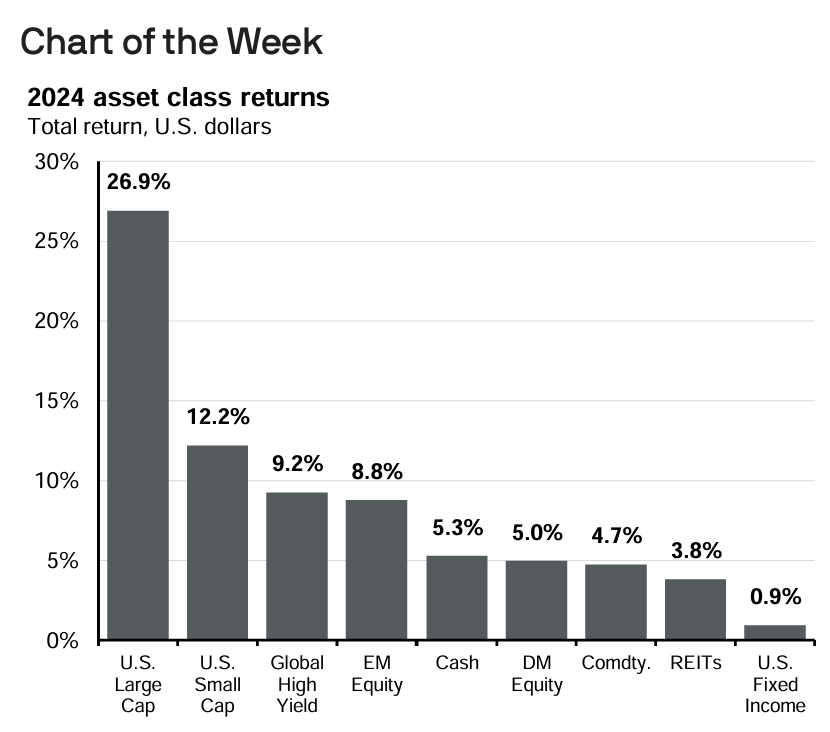

2024 saw strong returns overall, but with greater variability in performance across asset classes compared to 2023. Headlines were dominated by tragic conflicts, the U.S. election and soft vs. hard landing debates, but fundamentals remained the key driver of returns.

The clear winner was U.S. large-cap equities, achieving another year of 20%+ gains – a rare feat for the S&P 500, which has only seen consecutive 20%+ annual returns four times since 1900. Despite anticipated negative earnings growth, small caps climbed a solid 11.8%, fueled by optimism around deregulation and corporate tax cuts. Global high yield bonds benefited from central bank cutting cycles and low levels of defaults, rising 9.1%. EM equities had a better year, led by China’s impressive rebound following fiscal and monetary stimulus announcements in September and strong performances in Taiwan and India. On the other hand, DM equities lagged with only a 3.4% rise, hampered by yen and euro weakness and economic downturns in major eurozone markets. Despite the Fed’s rate cuts bringing down short rates, cash had its highest return since 2000. Next year should see more modest cash returns as the Fed continues its slow easing cycle. Commodity prices saw modest gains due to softening global demand. However, certain commodities like LNG and gold had robust returns, rising 67% and 27%, respectively. REITs rose 3.9%, constrained by elevated rates and sluggishness in office and retail sectors. Finally, U.S. fixed income finished the year on a down note, affected by economic resilience and elevated long rates, partly due to fiscal concerns.

This year's wide performance dispersion underscores the importance of rebalancing portfolios, as some sectors' impressive runs have left valuations high and susceptible to pullbacks.

*Source: J.P.Morgan Asset Management

Up Next

Next week's economic calendar will feature the Institute for Supply Management and S&P Global's US manufacturing sector data for December. Reports on pending homes sales for November and house price data for October are also due next week. Markets will be closed Wednesday for New Year's Day.

All the Best,

Gordon Achtermann, CSRIC®, MBA, CFP®

Gordon@yourbestpathfp.com

703-573-7325

Your Best Path Financial Planning delivers comprehensive planning and investment management to families and individuals, whether you live in Fairfax, Virginia, Northern Virginia, or nationwide.