Market Update 2025 Week 1

Market Recap 2024 Week 1

Dec. 30 through Jan. 3, 2025

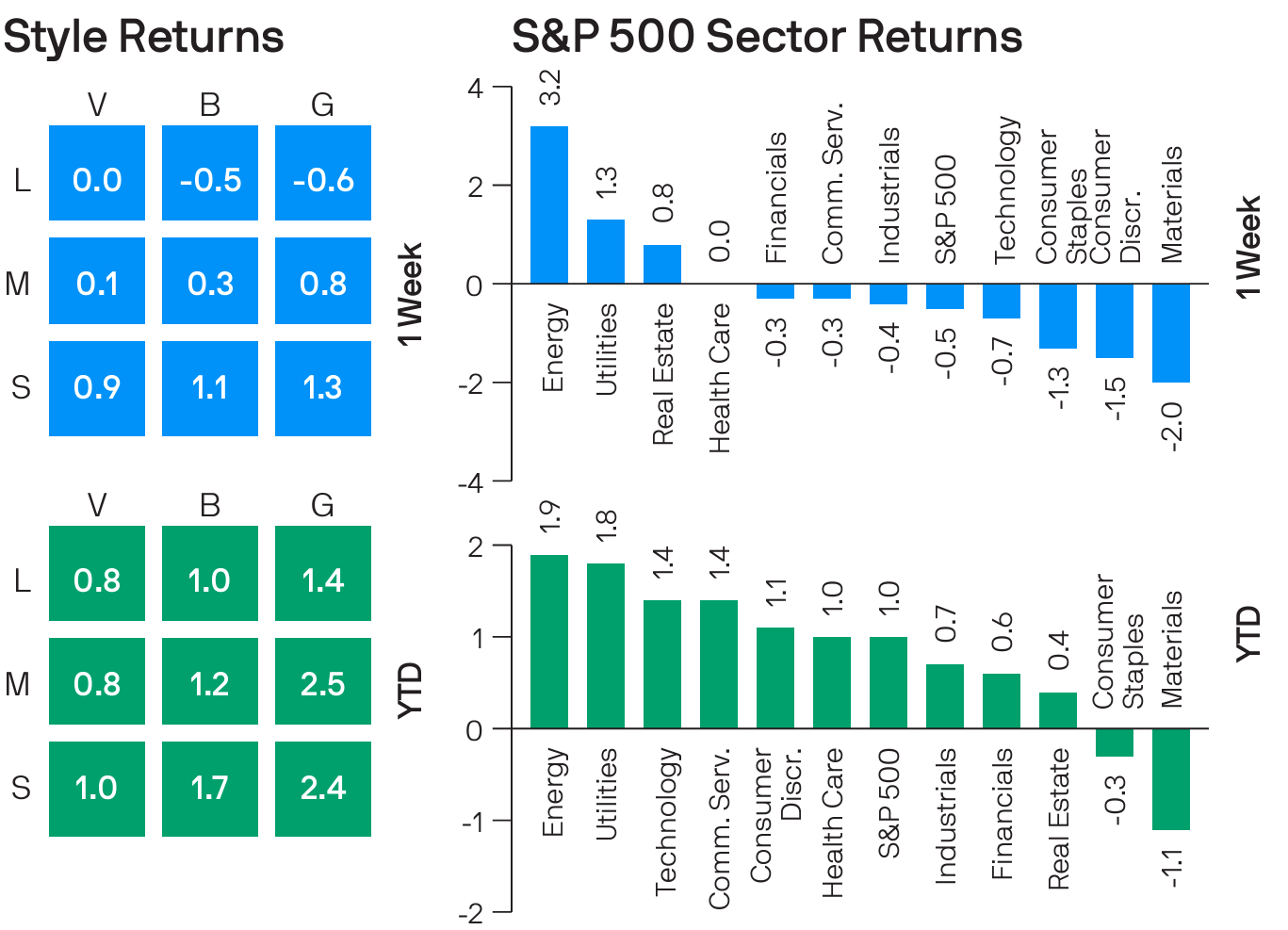

The S&P 500 index began the new year with a 0.5% weekly loss as the materials and consumer sectors declined, while energy and utilities stocks climbed.

The benchmark ended Friday's session at 5,942.47. The market was closed Wednesday for the New Year's Day holiday.

On Tuesday, the S&P 500 ended 2024 with a 23% annual gain. The index fell 2.5% in December.

This week, materials fell 2.1%, the biggest sector decline, followed by consumer discretionary dropping 1.5% and consumer staples with a 1.4% loss.

Thought of the Week*

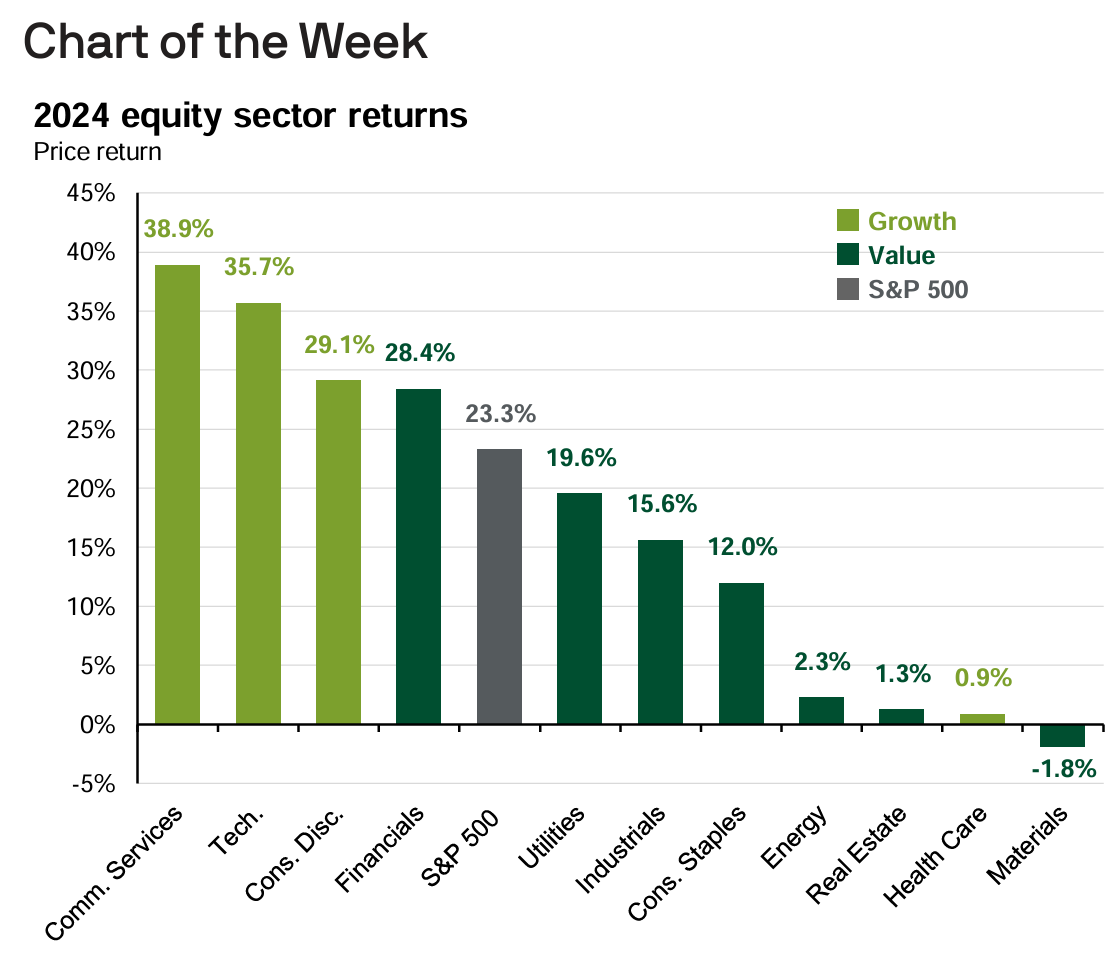

It was another great year for U.S. equities. The S&P 500 rose 23% and hit 57 new all-time highs along the way, the most since 1928. Once again, we have AI to thank for this spectacular performance. The Magnificent 7 rallied 48%, and for the second year in a row, technology, communication services and consumer discretionary were the top-performing sectors, while semiconductors & semiconductor equipment was the top-performing industry. Nevertheless, gains were slightly less concentrated: the Mag7 contributed 55% of the index return this year vs. 63% in 2023. This is partly due to an expanded recognition of AI beneficiaries. The utilities sector, for instance, rallied 20% this year as markets priced in elevated electricity demand from data centers. In fact, the second-best performing stock in the S&P 500 was an electrical utility.

But it’s not all about AI. After five consecutive quarters of contraction, earnings growth for the S&P 500 ex. Mag7 inflected positively in 2Q24. Financials, in particular, improved profitability as capital markets and commercial loan activity increased, supporting a 28% return for the sector. In 2025, broader earnings growth should drive broader leadership. We got a taste of this rotation in 3Q24 when value outperformed growth for the first time since 2022. Healthcare, however, has lagged throughout the year, partly due to a slower post-COVID earnings recovery, but mainly amid regulatory uncertainty. Despite entering October up 13%, it sold off 11% over the course of the fourth quarter. Indeed, markets will be watching Washington closely this year. Deregulation, tax and tariff policies could allelevate volatility. Investors should ensure tech’s outperformance hasn’t left portfolios unprotected or unprepared to capitalize on any resulting changes in leadership.

*Source: J.P.Morgan Asset Management

Up Next

Next week features December employment data, with ADP's monthly employment report expected on Wednesday and the Labor Department's employment report due on Friday. Other data on the calendar include November factory orders on Monday, December consumer credit on Wednesday and preliminary January consumer sentiment on Friday.

All the Best,

Gordon Achtermann, CSRIC®, MBA, CFP®

Gordon@yourbestpathfp.com

703-573-7325

Your Best Path Financial Planning delivers comprehensive planning and investment management to families and individuals, whether you live in Fairfax, Virginia, Northern Virginia, or nationwide.