Market Update Week 3

Market Recap 2024 Week 3

Jan. 13 - 17, 2025

The S&P 500 rose for the first time in three weeks on signs of easing inflationary pressures and strong earnings from major banks.

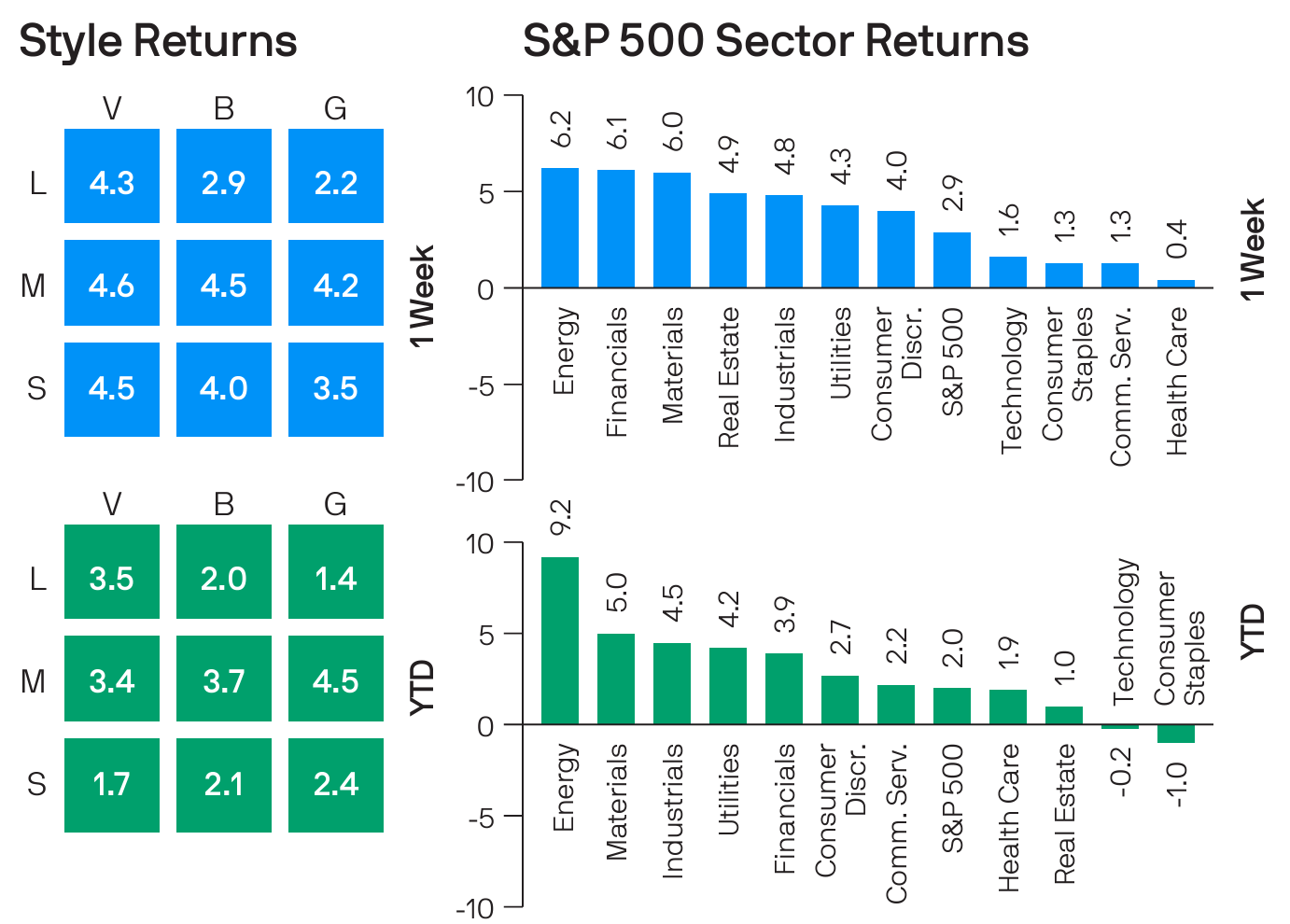

The benchmark equity index ended Friday's session 2.9% higher at 5,996.66, up from last week's close of 5,827.04. All sectors posted gains, led by financials and energy, up 6.1% each. Materials closed 6% higher.

Official consumer inflation data released this week showed core inflation, which excludes the volatile food and energy components, unexpectedly slowed in December.

"A somewhat benign reading in core consumer inflation on Wednesday coupled with a relatively cooler (producer price index) report on Tuesday offers welcome relief for a (Federal Reserve) increasingly concerned about an acceleration in cost pressures," Stifel said in a note to clients.

Retail sales rose at a slower-than-projected pace last month, while homebuilder confidence unexpectedly grew in January. Housing starts climbed more than expected last month.

Markets widely expect the Federal Open Market Committee to hold interest rates steady later this month, according to the CME FedWatch tool.

The International Monetary Fund raised its global and US economic growth expectations for this year but said the balance of risks to the overall outlook is tilted to the downside in the medium term.

It's interesting to see Value outperfrom Growth among the large-caps (3.5% to 1.4%), and mid-cap growth capture the most growth so far this year - 4.5%. A few weeks don't make a big trend, but we will keep an eye out to see how this develops.

Thought of the Week*

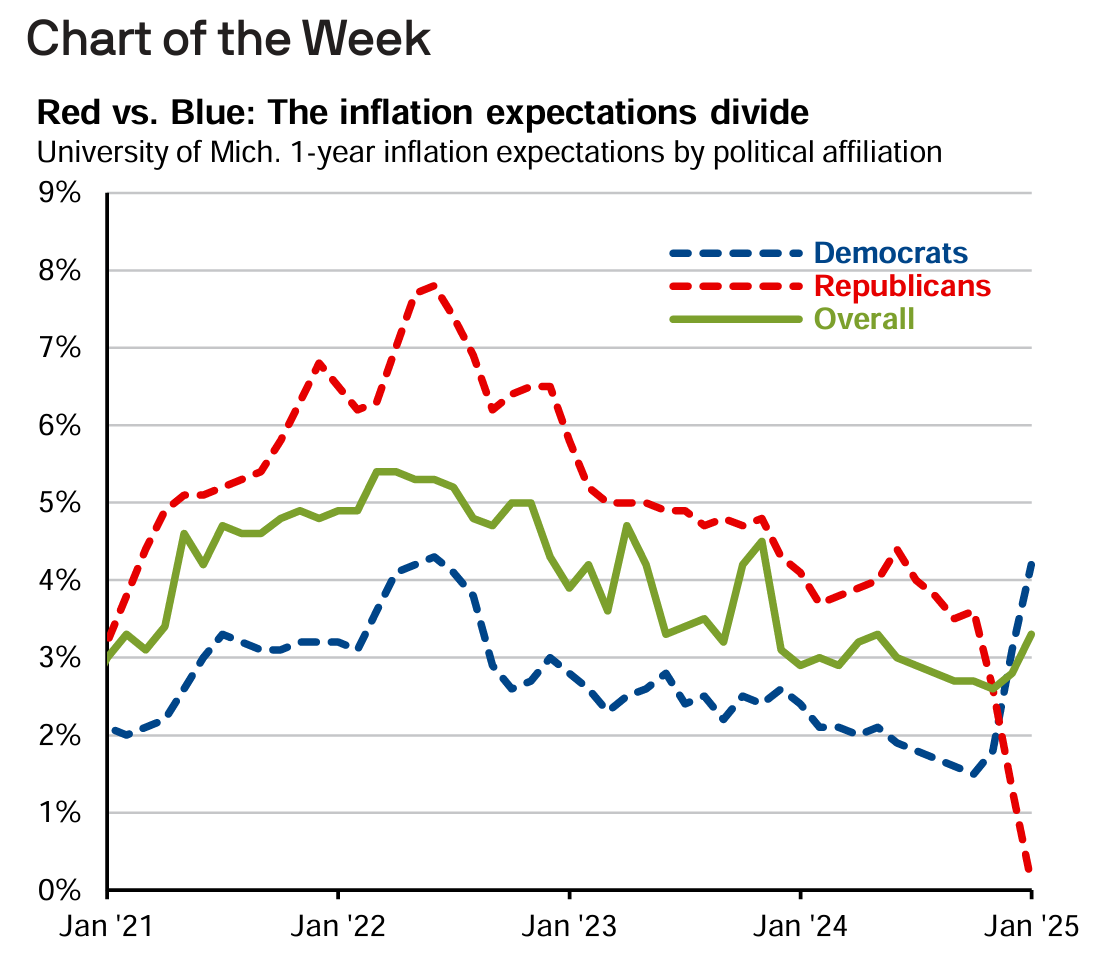

As President Trump begins his second term, the politically charged environment continues to shape consumer sentiment. The latest University of Michigan survey of inflation expectations revealed a sharp increase, with both one-year and five-year expectations jumping to 3.3% - levels last seen in May 2024 and June 2008, respectively. In contrast, December’s CPI report showed core inflation easing more than expected to 3.2% y/y. This disconnect has investors asking: why are consumer inflation expectations climbing despite signs of easing inflation, and what does it mean for investing?

To answer these, it is essential to separate the signal from the noise when interpreting survey data. Firstly, household inflation expectations are very volatile and highly sensitive to recent price changes in specific categories like gas (up 4.4% m/m in Dec.). Secondly, as the chart of the week shows, political bias heavily skews responses. Republicans expect inflation to nearly stall at 0.1% - a level the Fed considers unhealthy for economic growth - while Democrats forecast a surge to 4.2%, reflecting strong concerns about tariffs under the new administration. Lastly, consumer surveys often overestimate inflation outside major regime shifts, limiting their long-term reliability. On the other hand, professional forecasters have historically been more accurate. Their latest projection for year-ahead inflation remains at 2.3%, suggesting that not all political rhetoric will translate into policies and inflation will remain contained near the Fed’s target.

For investors, the takeaways are clear: don’t let political leanings influence investment decisions or distract from economic reality. Staying grounded with a well-diversified portfolio is essential to navigating the policy fog of 2025.

*Source: J.P.Morgan Asset Management

Personally, I think professional forecasters are wrong. As I write this, Trump is preparing to send troops to the southern border. Who do they think will pick vegetables and work in meat packing plants without illegal immigrants? If those places have to hire Americans, prices will triple, and productivity will plummet. Republicans who think that Trump can just force inflation to zero are in for a rude awakening. It will not be immediate, but it is inevitable.

Up Next

Next week's economic calendar will feature the existing home sales report for December and the University of Michigan's preliminary reading of consumer sentiment for January, both due Friday. Markets will be closed Monday in observance of Martin Luther King Jr. Day.

All the Best,

Gordon Achtermann, CSRIC®, MBA, CFP®

Gordon@yourbestpathfp.com

703-573-7325

Your Best Path Financial Planning delivers comprehensive planning and investment management to families and individuals, whether you live in Fairfax, Virginia, Northern Virginia, or nationwide.